01/07/2026

Mizuho Bank points out that the historic slump of the Japanese yen to multi-decade lows has completely broken the traditional interest rate pricing rules, forcing market investors to revamp their conventional trading strategies for the yen exchange rate.

For a long time, market strategists have relied on theJapan-U.S. interest rate differential to predict the USD/JPY exchange rate, which has long served as a core mainstream trading logic in the industry. Under normal market conditions, a rise in Japanese government bond yields relative to U.S. Treasury yields would effectively underpin the yen. However, this classic correlation has reversed in recent years: Japanese bond yields have continued to climb while the yen has weakened sharply. This abnormal divergence has also been observed in the currencies of some other G10 member economies.

Jordan Rochester, Head of EMEA Fixed Income, Commodities and Currency Strategy at Mizuho Bank, stated in a latest report that the changing correlation dynamics indicate the yen “no longer trades like a typical G10 currency”. He explained that the overhaul of the market’s pricing logic stems primarily from global market turbulence triggered by the Trump administration’s “Liberation Day” tariffs. The market has adjusted its hedging behaviours accordingly, while rising participation of overseas investors in Japan’s government bond market has further reshaped the yen’s pricing mechanism.

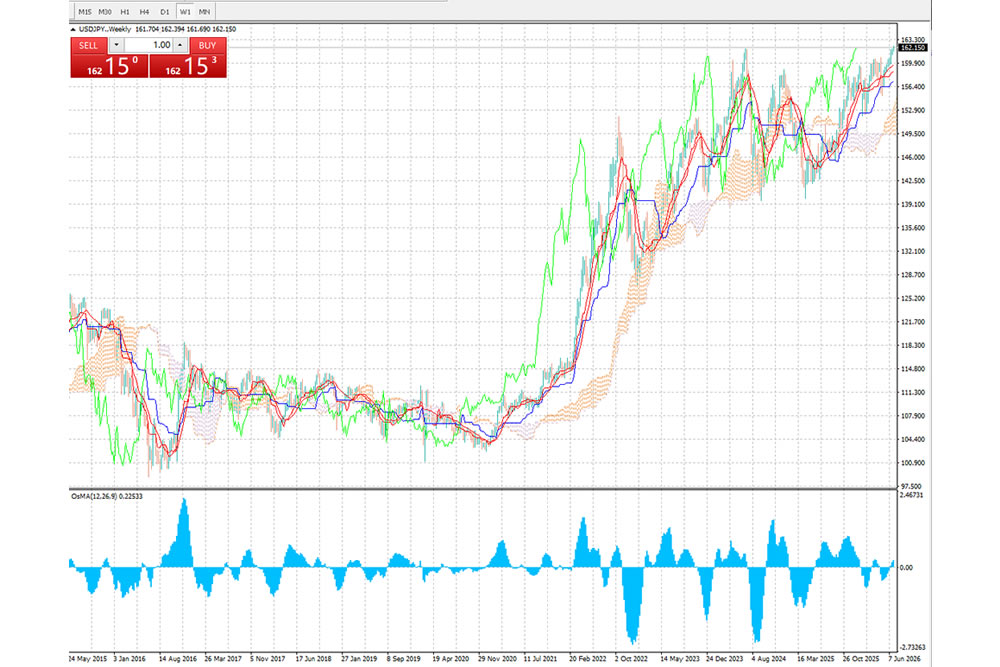

The yen has recently tumbled to its lowest level since 1986. On Tuesday, the USD/JPY pair broke above the 162 threshold. Previously, when the yen first fell below the key 160 level between April 28 and May 27, Japanese authorities intervened in the foreign exchange market with a record-breaking 11.73 trillion yen (approximately 72.1 billion U.S. dollars). Following this large-scale intervention, Japanese regulators have stayed on the sidelines and refrained from further market operations for a full month.

Market strategists now regard the 163 and above range as the next critical threshold for USD/JPY. The consensus view is that Japan’s Ministry of Finance has shown significantly higher tolerance for yen weakness compared with its intervention stance in 2024, and is likely to allow further moderate depreciation of the currency.

Meanwhile, Rochester cautioned that the shift in the yen’s trading pattern does not equate its performance to that of emerging market currencies. He cited historical G10 market moves as evidence that temporary decoupling between interest rates and exchange rates during market stress is not unprecedented. A notable example is the British pound during Liz Truss’s premiership, when sterling also deviated from traditional interest rate pricing logic and experienced exceptional volatility.

Rochester concluded that the yen has entered a new short-to-medium-term pricing regime. Investors must abandon their long-held conventional assumption that rising Japanese government bond yields will strengthen the yen, as traditional trading strategies based on Japan-U.S. interest rate differentials are no longer viable.

[Disclaimer] Forex trading involves risk; please invest with caution. This content is for informational purposes and objective analysis only, and does not constitute any investment advice, basis for buying/selling, or guarantee of returns. Investors should make independent decisions based on their own financial situation and risk tolerance, and bear their own investment risks.