30/06/2026

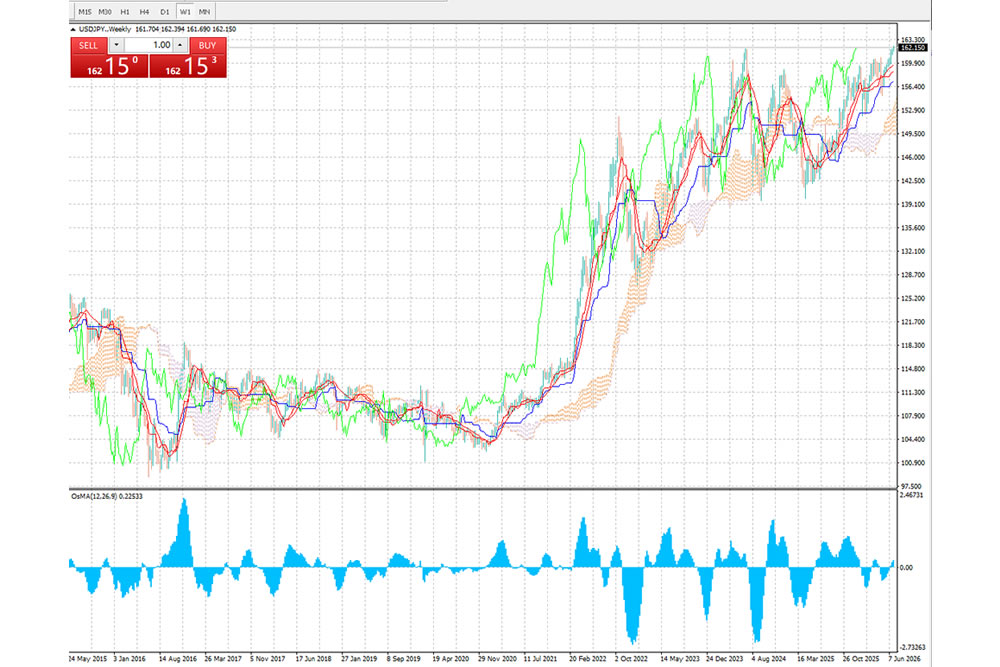

The Japanese yen has tumbled to a historic low, hitting its weakest level against the U.S. dollar since 1986. The unprecedented slump has triggered widespread unease across Japan and put global currency traders on high alert for official market intervention.

The yen’s downward momentum intensified during overnight New York trading, when it broke past 161.95 against the U.S. dollar, surpassing the previous low established in July 2024 during Japan’s official currency defense operations. The depreciation extended into Tuesday’s Tokyo trading session, with the yen falling further to 162.40. Neither public remarks from Chief Cabinet Secretary Minoru Kihara nor subsequent statements by Finance Minister Mayu Katayama managed to halt the persistent decline.

The last time the yen traded at such a depressed level, the currency was moving in the entirely opposite direction. Backed by U.S.-led monetary agreements in 1986, the yen embarked on a multi-year massive appreciation rally. The global and economic landscape at that time was vastly different: Japan was in the middle of an asset bubble expansion with robust economic growth, while the Soviet Union was still recovering from the aftermath of the Chernobyl nuclear disaster.

Decades later, Japan has long exited its economic boom and endured a generation-long period of stagnation. The latest sharp yen depreciation has delivered mixed and highly polarized impacts on the Japanese economy.

On the positive side, a weaker yen has significantly boosted the competitiveness of Japanese exporters and bolstered their corporate profits, driving Japan’s stock market to record highs. The country’s automotive sector stands out as a major beneficiary, with the weak yen expected to add up to 5.8 billion U.S. dollars in profits for Japanese automakers this year. According to Toyota’s estimates, every one-yen depreciation against the U.S. dollar increases the company’s operating profit by 50 billion yen, allowing major manufacturers to reap substantial and sustained gains from the currency’s weakness.

Nevertheless, the downsides of yen depreciation are far more prominent, severely squeezing household finances and undermining domestic economic stability. Largely reliant on imports for energy resources, Japan purchases most of its crude oil and natural gas in U.S. dollar terms. The plunging yen has drastically inflated import costs and fueled imported inflation. Prices across daily necessities, food products and electricity services have surged nationwide, eroding household purchasing power and putting growing pressure on consumers. The soaring cost of living has also weighed heavily on the approval rating of Prime Minister Sanae Takachi’s administration.

Notably, the yen’s relentless slump has defied market expectations, occurring amid a pivotal shift in Japan’s monetary policy. Following a leadership change at the Bank of Japan (BOJ), the country terminated its long-standing negative interest rate policy. On June 16, the BOJ raised its benchmark interest rate to 1%, the highest level since 1995. Despite hopes that the policy tightening would revitalize the yen, the rate hike has produced minimal uplifting effects on the currency.

The core driver behind the continued depreciation is the widening interest rate gap between Japan and the United States. Market participants widely expect the Federal Reserve to maintain a hawkish monetary stance for an extended period, keeping U.S. interest rates significantly higher than Japan’s ultra-low rates. This encourages investors to borrow yen at low costs and channel capital into higher-yield overseas assets. The resulting persistent capital outflows have continued to weigh heavily on the yen, offsetting the BOJ’s tightening measures entirely.

Furthermore, market concerns over a slowdown in Japan’s future rate hikes have added downward pressure on the yen. Signs indicate the Japanese government intends to temper the BOJ’s tightening pace, with its new basic policy guidelines calling for flexible and moderate monetary management, which greatly limits the room for aggressive rate hikes.

Japanese authorities have already intervened heavily in the foreign exchange market yet failed to reverse the bearish trend. Official data shows Japan launched a record-scale intervention between April 28 and May 27, injecting 11.73 trillion yen (approximately 72.4 billion U.S. dollars) to prop up the currency. Reserve figures from the Ministry of Finance confirm that the intervention utilized foreign securities including U.S. Treasury bonds for yen-buying operations, yet the currency continued to weaken.

The massive intervention effort lays bare Japan’s daunting challenge: it is extremely difficult for a single nation to counteract prevailing market trends in the global foreign exchange market, which sees a daily trading volume of 9.5 trillion U.S. dollars. Even substantial state-led capital intervention can barely turn the tide against powerful market forces.

Beyond the key interest rate differential, a combination of external and structural domestic factors continues to suppress the yen’s value. Externally, this year’s military tensions between the U.S. and Iran have compounded pressure on the yen. As Japan relies almost entirely on Middle Eastern oil imports, regional geopolitical turbulence poses acute risks to its energy supply and currency stability. Although de-escalation talks have eased global oil price volatility, the yen’s downtrend has persisted, proving that structural factors such as interest rate gaps remain the dominant drivers.

Domestically, deep-rooted structural economic flaws continue to constrain the yen’s long-term outlook. Japan’s aging and shrinking population dampens long-term growth prospects and contributes to ballooning public debt. These fundamental challenges have convinced markets that Japan cannot afford aggressive or rapid interest rate hikes, locking the yen in a prolonged weak pattern.

Facing the unchecked currency depreciation, Japanese officials have maintained a firm stance on market stabilization. On June 19, Finance Minister Mayu Katayama reiterated that authorities stand ready to take bold action to curb excessive speculation in the foreign exchange market. She also stated that Japan and the United States have aligned their foreign exchange policies following her communication with U.S. Treasury Secretary Scott Bessent, agreeing to adopt decisive measures to address currency volatility when necessary.

In terms of intervention history, Japan resumed currency market intervention in 2022 for the first time since 1998 and stepped in again repeatedly in 2024. Each official intervention only delivered temporary relief, with the yen quickly resuming its downward trajectory. The multiple rounds of intervention launched since April 30 this year have merely slowed the slump marginally without reversing the overall bearish trend.

Market focus has now shifted to further downside targets. Having broken the critical 1986 support level, the yen is now facing a potential slide toward the 164–165 range against the U.S. dollar. An accelerated depreciation would trigger strong market expectations of another large-scale yen-buying intervention by Japanese authorities, emerging as the biggest uncertainty in the current foreign exchange market.

[Disclaimer] Forex trading involves risk; please invest with caution. This content is for informational purposes and objective analysis only, and does not constitute any investment advice, basis for buying/selling, or guarantee of returns. Investors should make independent decisions based on their own financial situation and risk tolerance, and bear their own investment risks.